The Death of the “Standard” 30-Year Fixed Mortgage Model

The Macro Problem

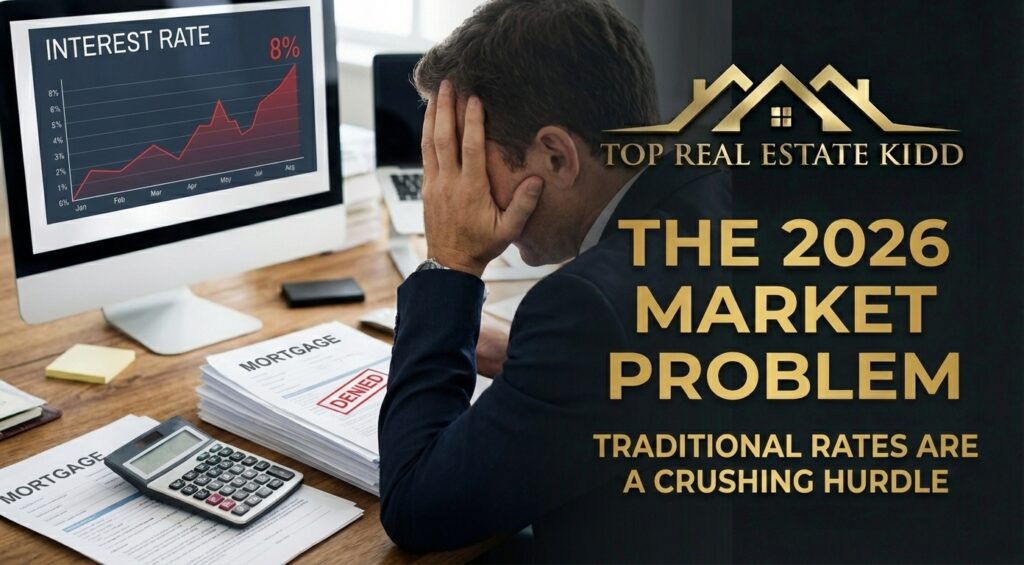

The 2026 real estate market has hit a massive, systemic bottleneck. For the average buyer, the traditional path to homeownership hasn’t just become more expensive—it has become mathematically impossible.

With bank interest rates currently sitting at a “sticky” 8%, the purchasing power of the American family has been slashed by nearly 40% compared to just a few years ago. This isn’t just a “high rate” problem; it’s a “Cost of Capital” crisis.

The Crushing Hurdle:

When interest rates move from 3% to 8%, the interest paid over the life of a $500,000 loan jumps from roughly $258,000 to over $820,000. That is over half a million dollars in pure interest expense that adds zero value to the home. This “Rate Wall” is forcing buyers to settle for smaller homes in lesser locations, or worse, stay on the sidelines indefinitely.

The Stagnant Supply:

On the other side of the hurdle, sellers are “locked in” to their current 3% rates. They can’t afford to sell and trade up to an 8% mortgage, creating a frozen market with record-low inventory.

Conclusion:

In 2026, if you are playing the traditional bank game, you are losing. The market is waiting for a disruptor.